Our Main Office

Construction Equipment Guide

470 Maryland Drive

Fort Washington, PA 19034

800-523-2200

Wed October 31, 2018 - National Edition

United Rentals, Inc. announced that it has completed its previously announced acquisition of BlueLine from Platinum Equity for a total purchase price of approximately $2.1 billion in cash. The company used a combination of newly issued debt and bank borrowings to fund the transaction and related expenses.

The acquisition expands United Rentals' equipment rental capacity in many of the largest metropolitan areas in North America, including both U.S. coasts, the Gulf South and Ontario. The company gains a well-diversified customer base with a balanced mix of commercial construction and industrial accounts, over 46,000 rental assets, 114 branch locations and approximately 1,700 employees.

Michael Kneeland, chief executive officer of United Rentals, said, "We're excited to welcome BlueLine to the United Rentals family, and we're confident that the strategic and financial merits of the acquisition will benefit our customers, shareholders and employees. Moreover, we look forward to leveraging our extensive integration capabilities to ensure that we generate the greatest value from combining our companies. Together, our enhanced scale and operating efficiencies reinforce our leadership position in the North American market and support our focus on driving long-term value creation."

Louis Samson, partner at Platinum Equity, said, "The combination with United Rentals is the optimal conclusion to our BlueLine investment. We're extremely pleased with this transaction and the opportunities created for the BlueLine team and customers. It's fitting that their next phase of growth will be with the industry leader."

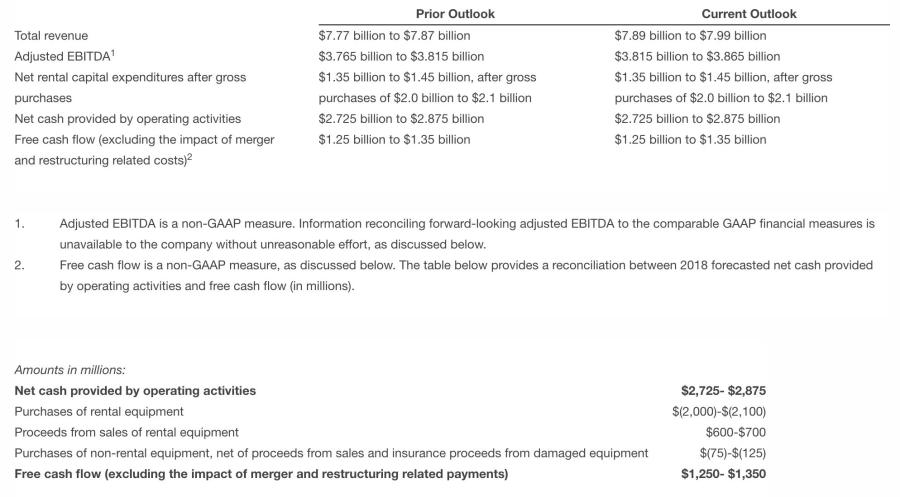

The company has updated its full-year 2018 guidance solely to reflect the expected impact of the BlueLine acquisition. The new guidance adds $120 million of total revenue and $50 million of adjusted EBITDA to the guidance previously released on October 17, 2018:

Morgan Stanley & Co. LLC and Centerview Partners acted as financial advisors to United Rentals, and Sullivan & Cromwell LLP acted as legal advisor. Barclays and Catalyst Strategic Advisors acted as financial advisors to Platinum Equity, and Latham & Watkins LLP acted as legal advisor.

As previously announced, United Rentals has paused its current $1.25 billion share repurchase program effective with the BlueLine closing, consistent with recent larger acquisitions. Once the initial phase of the integration is complete, the company will re-evaluate its decision to pause the repurchase program with the intention of completing the balance of the authorization.

Free cash flow and adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) are non-GAAP financial measures as defined under the rules of the Securities and Exchange Commission. Free cash flow represents net cash provided by operating activities less purchases of, and plus proceeds from, equipment. The equipment purchases and proceeds represent cash flows from investing activities. EBITDA represents the sum of net income, provision for income taxes, interest expense, net, depreciation of rental equipment and non-rental depreciation and amortization. Adjusted EBITDA represents EBITDA plus the sum of the merger related costs, restructuring charge, stock compensation expense, net and the impact of the fair value mark-up of acquired fleet. The company believes that: (i) free cash flow provides useful additional information concerning cash flow available to meet future debt service obligations and working capital requirements; and (ii) adjusted EBITDA provides useful information about operating performance and period-over-period growth and help investors gain an understanding of the factors and trends affecting our ongoing cash earnings, from which capital investments are made and debt is serviced. However, neither of these measures should be considered as alternatives to net income or cash flows from operating activities under GAAP as indicators of operating performance or liquidity.

Information reconciling forward-looking adjusted EBITDA to GAAP financial measures is unavailable to the company without unreasonable effort. The company is not able to provide reconciliations of adjusted EBITDA to GAAP financial measures because certain items required for such reconciliations are outside of the company's control and/or cannot be reasonably predicted, such as the provision for income taxes. Preparation of such reconciliations would require a forward-looking balance sheet, statement of income and statement of cash flow, prepared in accordance with GAAP, and such forward-looking financial statements are unavailable to the company without unreasonable effort. The company provides a range for its adjusted EBITDA forecast that it believes will be achieved, however it cannot accurately predict all the components of the adjusted EBITDA calculation. The company provides an adjusted EBITDA forecast because it believes that adjusted EBITDA, when viewed with the company's results under GAAP, provides useful information for the reasons noted above. However, adjusted EBITDA is not a measure of financial performance or liquidity under GAAP and, accordingly, should not be considered as an alternative to net income or cash flow from operating activities as an indicator of operating performance or liquidity.

Construction Equipment Guide

470 Maryland Drive

Fort Washington, PA 19034

800-523-2200

Construction Equipment Guide covers the nation with its four regional newspapers, offering construction and industry news and information along with new and used construction equipment for sale from dealers in your area. Now we extend those services and information to the internet. Making it as easy as possible to find the news and equipment that you need and want.

Contents Copyrighted 2025, by Construction Equipment Guide, which is a Registered Trademark, registered in the U.S. Patent Office. Registration number 0957323. All rights reserved, nothing may be reprinted or reproduced (including framing) in whole or part without written permission from the publisher. All editorial material, photographs, drawings, letters, and other material will be treated as unconditionally assigned for publication and copyright purposes and are subject to Construction Equipment Guide’s unrestricted right to edit and comment editorially. Contributor articles do not necessarily reflect the policy or opinions of this publication.

Read our privacy policy here.

Mastodon